Bank Locker Policy

- lightgrey-pony-400654.hostingersite.com

- Bank Locker Policy

Total Cover

100% Claim Settlement

No

Documentation

Reasonable

Premium

Total Cover

100% Claim Settlement

No

Documentation

Reasonable

Premium

Our Proud Partners - Beemawala

Client Testimonials

What is Bank Locker Policy ?

A Bank Locker Policy is an insurance policy that provides coverage for the contents of a bank locker against risks like theft, fire, natural disasters, and more. It ensures financial protection for valuable items, documents, and assets stored in the locker. In the event of covered incidents, the policyholder receives compensation for the loss or damage to the stored items. Bank Locker Insurance offers peace of mind and a safeguard against unexpected events that could jeopardize the security of valuable belongings stored in a bank’s safe deposit box.

Coverages of Bank Locker Policy

Theft or Burglary

Coverage for loss or damage to the contents of your bank locker due to theft or burglary

Fire and Natural Calamities

Protection against damage or loss caused by fire, earthquakes, floods, storms, or other natural disasters

Terrorism

Coverage for losses resulting from acts of terrorism, which may include damage or destruction of your locker’s contents

Riot and Strike

Compensation for damage or loss during riots, strikes, or civil unrest situations.

Loss of Valuables

Reimbursement for the loss of valuable items such as jewelry, documents, cash, and other assets stored in the locker.

Legal Liability

Coverage for any legal liabilities arising from loss or damage to the contents of your locker.

Optional Add-Ons

Additional coverage options might include coverage for loss of documents, electronic data, or items of high value.

Additional Add-ons of Bank Locker Policy

Cash Cover

Provides additional coverage specifically for cash stored in your locker, especially if it exceeds the standard policy limit.

Document Protection

Extends coverage to important documents stored in the locker, such as property deeds, wills, or financial records.

Specialized Jewelry Coverage

Offers higher coverage limits or better terms for valuable jewelry items.

Specific Item Coverage

Allows you to specify and insure individual high-value items separately, ensuring comprehensive protection for these items.

Factors Determining the Premium of Bank Locker Insurance Policy

- Several factors influence the premium of a Bank Locker Insurance policy:

Coverage Limit

The higher the coverage limit you choose, the more you’ll pay in premiums. It’s essential to select a coverage limit that adequately reflects the total value of the items stored in your locker.

Location

The location of the bank where your locker is situated can affect the premium. Locker facilities in areas prone to theft or natural disasters may have higher premiums.

Security Measures

The level of security provided by the bank can impact your premium. Banks with advanced security systems and surveillance may offer lower premiums.

Claim History

Your past claims history can impact the premium. Frequent claims may result in higher costs.

Policy Term

The duration of your policy term also plays a role. Longer-term policies may have lower annual premiums.

Major Differences Between Bank Locker Insurance policy and Home Insurance policy

| Aspect | Bank Locker Insurance Policy | Home Insurance Policy |

|---|---|---|

Coverage |

Covers valuables stored in a bank locker. |

Covers the structure of your home and its contents. |

Location

|

Limited to the insured bank locker. |

Provides coverage for your home, regardless of its location. |

Insured Items

|

Valuables and assets stored in the locker. |

Building structure, personal belongings, and liability coverage. |

Premium Factors |

Based on locker size, value of stored items, and location. |

Based on property value, location, construction type, and coverage type. |

Access Control

|

Focuses on security measures related to bank lockers. |

Addresses home security, including alarms, locks, and surveillance. |

Add-Ons and Riders |

May offer add-ons for extended coverage of valuable items. |

Offers various riders like personal property, earthquake, or flood insurance. |

Deductible |

Usually low or zero deductible. |

Varies based on policy and insurer, often with options to adjust. |

Claim Types |

Primarily theft or damage to items in the locker. |

Covers a wide range of perils, including theft, fire, natural disasters, and more. |

Policy Duration |

Typically annual policies. |

Can be annual or multi-year policies. |

Policy Customization |

Tailored to specific locker contents. |

Offers customization options based on property and personal belongings. |

Liability Coverage |

Not applicable; focuses on asset protection. |

Includes personal liability coverage for accidents or damage to others. |

Property Location |

Applies specifically to the bank locker. |

Covers property at its designated location (e.g., your home). |

Premium Cost |

Generally lower due to limited scope. |

Can be higher due to broader coverage and property valuation. |

Coverage Scope in Emergencies |

Protects valuable assets in the event of theft or damage at the bank. |

Provides a comprehensive safety net for homeowners in various emergencies. |

How to Settle Bank locker Insurance Policy

Notification

As soon as you discover the loss or damage to the insured items in your bank locker, notify the insurance company immediately. Most insurers have a dedicated claims hotline or an online portal for claim intimation.

Claim Form

Complete the claim form provided by the insurance company. Ensure accuracy and honesty in all details provided.

Supporting Documents

Gather all the supporting documents required by the insurer. These may include a copy of the FIR (First Information Report) filed with the police, the bank’s report confirming the incident, your policy documents, photographs of the damaged items, and any other documents requested by the insurer.

Assessment

The insurance company will assess the claim based on the information and documents provided. They may also send a claims adjuster or surveyor to evaluate the loss.

Verification

The insurer may verify the details with the bank where the locker is located to corroborate the incident.

Settlement Offer

Once the assessment is complete, the insurer will make a settlement offer based on the terms and conditions of your policy and the assessed value of the loss. You have the option to accept or negotiate the offer.

Acceptance

If you accept the offer, the insurer will initiate the settlement process. This may involve compensation in the form of a monetary payout or replacement of items, depending on your policy terms.

Dispute Resolution

In case of disputes or disagreements regarding the claim settlement, you can follow the insurer’s complaint resolution process or seek assistance from the insurance ombudsman if necessary.

Claim Settlement

Upon agreement, the insurer will release the settlement amount or provide replacements as per the policy terms.

Claim Closure

Once the settlement is complete, the claim is considered closed.

Exclusions of Bank Locker Insurance Policy

Loss Due to War or Terrorism

Policies typically exclude losses caused by war, civil war, or acts of terrorism. Damage or theft of items from your bank locker due to such events will not be covered.

Unexplained Disappearances

If items in your bank locker disappear without any evidence of theft or damage, they may not be covered. Most policies require proof of theft or damage.

Nuclear Contamination

Loss or damage caused by nuclear contamination, radiation, or radioactive material is usually excluded.

Illegal Activities

If the loss or damage occurs as a result of illegal activities, such as storing stolen goods in your locker, it won’t be covered.

Wear and Tear

Bank Locker Insurance typically doesn’t cover wear and tear, depreciation, or gradual deterioration of items.

Inadequate Security Measures

If you fail to take reasonable security measures as specified in your policy, like not following the bank’s locker access procedures, it might lead to claim denial.

Items Not Declared

Any items not declared to the insurance company during the policy issuance or additions made later may not be covered.

Policy Violations

Violating policy terms, such as not paying premiums on time, can result in a loss of coverage.

Loss Outside Policy Territory

Some policies may not cover losses that occur outside the geographical territory specified in the policy.

Unauthorized Access

Loss or damage caused by someone who had unauthorized access to your locker, like a bank employee without proper authorization, may not be covered.

Items in Circulation

Items that are currency notes, coins, and negotiable instruments in circulation may be excluded.

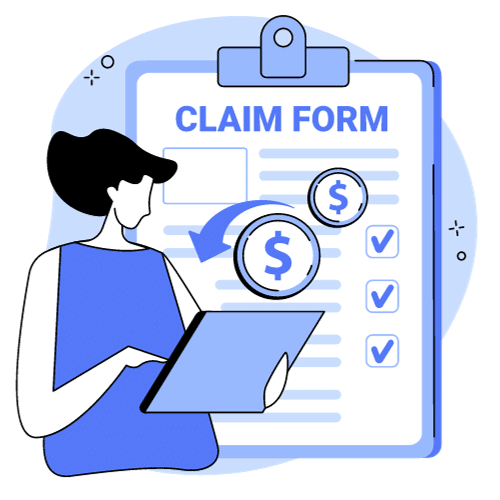

Documents Required for Claim Settlement under Bank Locker Insurance Policy

Claim Form

You must fill out a claim form provided by the insurance company. This form will require you to provide essential details about the claim, including the incident’s date, description, and the items lost or damaged.

FIR (First Information Report)

In case of theft or burglary, you’ll need to file an FIR with the local police station and provide a copy of the FIR to the insurer as proof of the incident.

Bank Locker Agreement

Submit a copy of the bank locker agreement or rental receipt, which proves that you had a valid locker with the bank.

Inventory List

Prepare an inventory list of the items stored in the locker. Include details such as item descriptions, values, purchase receipts, and photographs if available.

Valuation Certificates

Provide valuation certificates or appraisals for high-value items or jewelry, as these documents help in determining the items’ worth.

Bank Confirmation

The bank might need to confirm the details of the incident and the condition of the locker. The insurance company may require an official letter from the bank.

Identity Proof

Your identity proof, such as a copy of your Aadhar card, PAN card, or passport, may be needed for verification.

Address Proof

A proof of address, like a utility bill or a rental agreement, may be required for correspondence and verification.

Photos

If possible, provide photographs of the damaged items or the condition of the locker after the incident.

Bank Statemen

A bank statement showing the locker rental charges and deductions (if any) can support your claim.

Any Other Relevant Documents

Depending on the circumstances, the insurer may request additional documents for claim assessment.

Contact Information for Claim Settlement: Under Construction Building Insurance Policy

If Policy Obtained through Agent/Broker

If Policy Obtained Directly from Insurance Company

Claim Contact Information for Policy from Beemawala.com

If you have taken the policy from Beemawala.com, please use the following contact details to register your claim.

- Phone: +91-9654259715

- Email: services@lightgrey-pony-400654.hostingersite.com

Frequently Asked Questions: (FAQs) on Bank Locker Insurance Policy

Contact your insurance provider immediately after the incident. Provide necessary documents like the FIR in case of theft or relevant evidence for other claims.

Popular Other Fire-related Insurance Options in India

- Click Below for Other Fire-related Insurance Policy